Task: CONTRIBUTING TO THE STRATEGY

Type: DIGITAL STRATEGY

Role: SUBJECT MATTER EXPERT

Duration: SUMMER/FALL 2019

SUMMARY

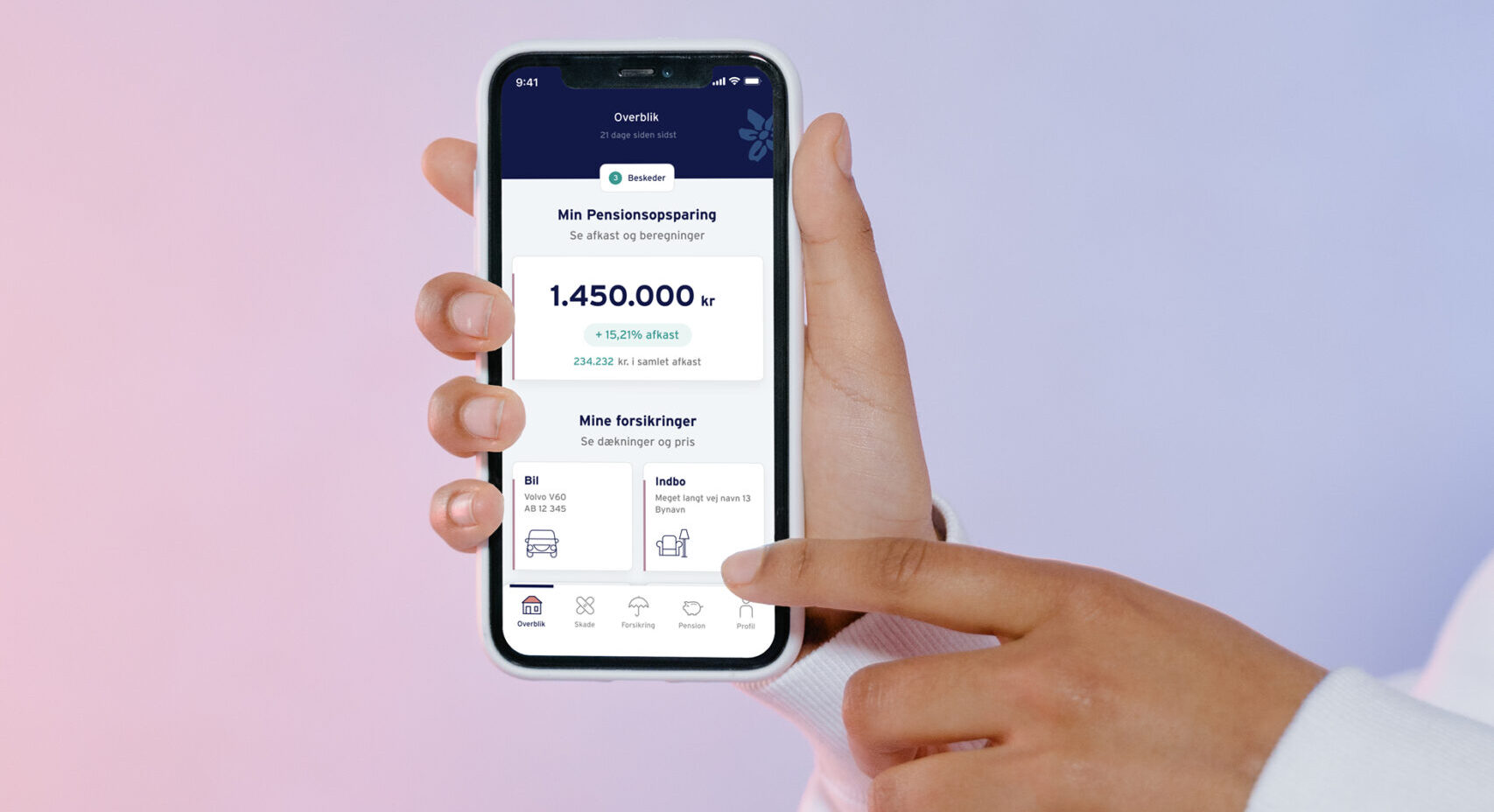

Having a crucial role in developing and executing Nordea’s digital strategy (called FLOW) with the ambition of creating financial well-being for all 10 million customers across the Nordics. This includes facilitating the process of turning the strategy into tangible concepts and UX initiatives within the area of savings and investment. My focus in this project was to make savings and investment relevant and transparent for Nordea's customers when they interact with the bank digitally.

On the surface, people’s relationship with money appears straightforward. Digital banking services have made it easier than ever to make payments, check balances, and access your financial data. However, the reality is slightly different. It shows that people struggle with having a comprehensive overview of their finances. This headache produces a series of questions; Am I spending too much? How do I best plan for retirement? Does my insurance cover my family's needs?

From work deadlines and terrorism to social pressures and health issues, people still worry more about their finances, which is damaging to their overall wellbeing.

Financial stress is rooted in a lack of full overview and context which triggers feelings of frustration and loss of control. Everyone wants to have financial peace of mind, the assurance that everything is all right today and tomorrow. Financial institutions - like Nordea - have both a great opportunity and a major responsibility to help people who are suffering from financial stress. According to Red Associates, the biggest barrier for financial institutions seeking to build meaningful customer relationships is demonstrating how digital can support the marriage of people’s fast- and slow money.

In short, how can Nordea provide digital tools and services that help the customers to get a comprehensive overview of their financial situation and create financial well-being?

The outcome of this project is to take the key insights of the strategy and turn them into an actionable roadmap that Product Managers, Product Owners, and the rest of the agile setup easily can tap into and prioritize in their planning sessions. Before jumping to conclusions it's important to understand the steps in between.

Let's start with the definitions of slow and fast money, which is the foundation of the strategy. Fast money (bill payments, daily expenditures, bank accounts, etc.) are used in and assigned to the present and near future; it is engaged with on a regular basis, and its management is often digital. Slow money (pensions, insurance, investments, etc.) is assigned to some distant future purpose and is vastly more difficult for customers to manage and comprehend.

The philosophy behind the FLOW strategy is to bridge the gap between thinking isolated on either short or long-term money matters. Why? By creating a connection between fast and slow money you are creating an overview of your financial situation. Once you have a financial overview you are one step closer to achieve financial well-being.

Let's start with creating the connection between slow and fast money. Here is some kind of glue needed, which in this case is represented as 'Moderate money'. Moderate money consists of different types of savings.

Why is saving the glue? Financial products have historically focused on tools and services that expose historical data you cannot act on. Instead, financial products should simply facilitate actions in real life that can impact your future. When you start saving for something you are basically starting to have an impact on your financial future.

A useful framework to examine this convergence is a timescale of the customers' financial future mindset, from what I need to do today to the some-day category most never worry about decades into the future.

The main take away from the framework above is the customers' three types of mindsets and their connection to fast money, moderate money, and slow money;

Spend = Fast money

The purpose of this type of money is to make sure you can pay rent, buy groceries and cover other day-to-day spendings. The money often leaves your account quite quickly compared to the two other categories.

Moderate money = Save money

Unexpected expenses will happen and without an emergency fund in place, you’ll struggle to pay for them. Saving money for a rainy day helps you to maintain your lifestyle. This kind of money is stored in your account for a longer time period and your regular contributions make the pile of money grow.

Slow money = Grow money

Why not let your money work for you? By investing in property, material goods, or stocks you can let the money do the hard work. In other words, your pile of money grows - even without regular contributions. The time horizon is not just around the corner so the money stays in your account for a pretty long time.

If you as a customer don't want to live paycheck to paycheck it's essential to create a flow of money between the three bobbles illustrated below. This will bring you to a much more comfortable financial situation. This will also help you with the financial overview.

The movements of money within the area of savings and investment can basically be translated into three tracks viewed from the business perspective; Investments for investors, Investments for non-investors, and savings goals.

Investments for non-investors

ddf

- Guidance in an actionable format directly on the home screen, nudging users towards investing.

- Wizard-type flows for setting up the investment plans.

- Possibility to opt-out, or dismiss these if not interested to be defined.

User test feedback: People interested in investing, but with little or no knowledge of it thought the investment guidance was appealing and useful. They also confirmed this could lower their threshold for starting investing.

Investments for investors

- All investments are easily accessible from the home screen.

- Search and inspiration

- Automated investments

- An activity section monitors all the activities related to your investments like annual reports, dividends, transactions, orders, etc.

User test feedback: People interested in investing want to see how their holdings are performing in an easy overview - like the presented screens.

Savings goals

- A more accessible and fun way to save money.

- Create savings goals and apply savings rules to them to customize your unique personal savings plans.

- Follow the progress towards the goal.

User test feedback: This feature was met with enthusiasm. The participants found it very useful when trying to save for a specific purpose. The possibility to set up own rules for saving was also met with interest since it makes it easier, fun, and more convenient to manage.

..

Research & Insights phase consisting of customer interviews and desk research

Experience Framework Creation with add-ons to Red Associates' concept of slow money and fast money

Vision a prototype (App) with different concepts created from the themes.

Validating the strategy by testing the prototype

Other projects

Behaviour typesUser Research

Savings GoalsConcept Development

Onboard non-investorsDigital Strategy

Nordea MobileApp Design

Topdanmark AppApp Design

Nordea Online BankingWeb Design

Automated savingsConcept development